🌐 Inflation Fears Rise. Paper Supply Falls.

Building better understanding of global supply chain woes...and subsequent inflation.

Author’s note (2021)

The following was written prior to news about issues with the transportation system making it harder to get goods across the international economy. These delays only exacerbate the delays in the analysis below, making the impacts of the time delays described here even worse. This is what we’re experiencing.

Author’s note (2025)

Since this article was written, the world experienced long term inflation — as expected. The US managed to bring inflation under control faster. The analysis still holds regarding structural causes of supply / demand imbalances and inflation.

NY Times Headline: The World Is Still Short of Everything. Get Used to It.

US News Headline: Delta, Inflation Fears Push Consumer Sentiment Down Sharply in August

If you tune in to the Sunday morning economic pundits you’ll hear differing opinions about inflation. It’s here. It’s coming. It’s the current President’s fault. No, it’s the previous President’s. What’s going on?

Meanwhile…

A writer friend of mine—excited to be publishing their third book—lamented the other day, “I never thought I’d try to sell a new book in a time when printing paper was hard to find.” You’d think in a digital age there would be plenty of paper. Why the paper shortage? (Just today, Costco announced a purchase limit for toilet paper similar to 2020’s.)

Perhaps most important of all: How might these seemingly disparate issues be related?

SYSQ CAN ILLUMINATE

Systemic Intelligence (SysQTM) is the capacity to frame and analyze issues in ways that can generate maximum insight—which is the only way to identify optimal solutions. One of the core principles of SysQ is to Build a Shared Map of the territory of interest—a picture of the systemic structure driving the system’s performance. Another principle is to Focus on the Physics—make sure the map’s proposed causal connections are consistent with reality.

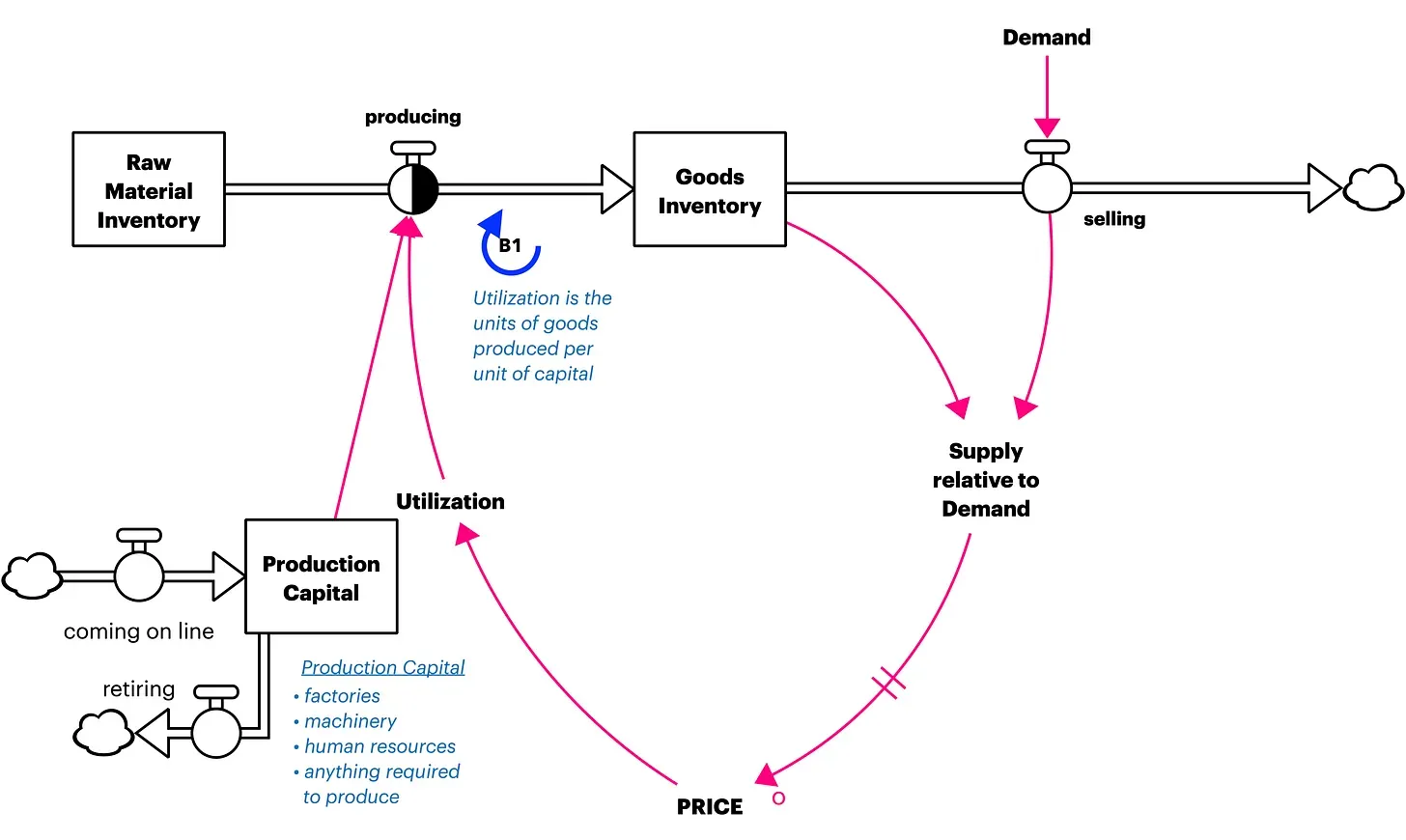

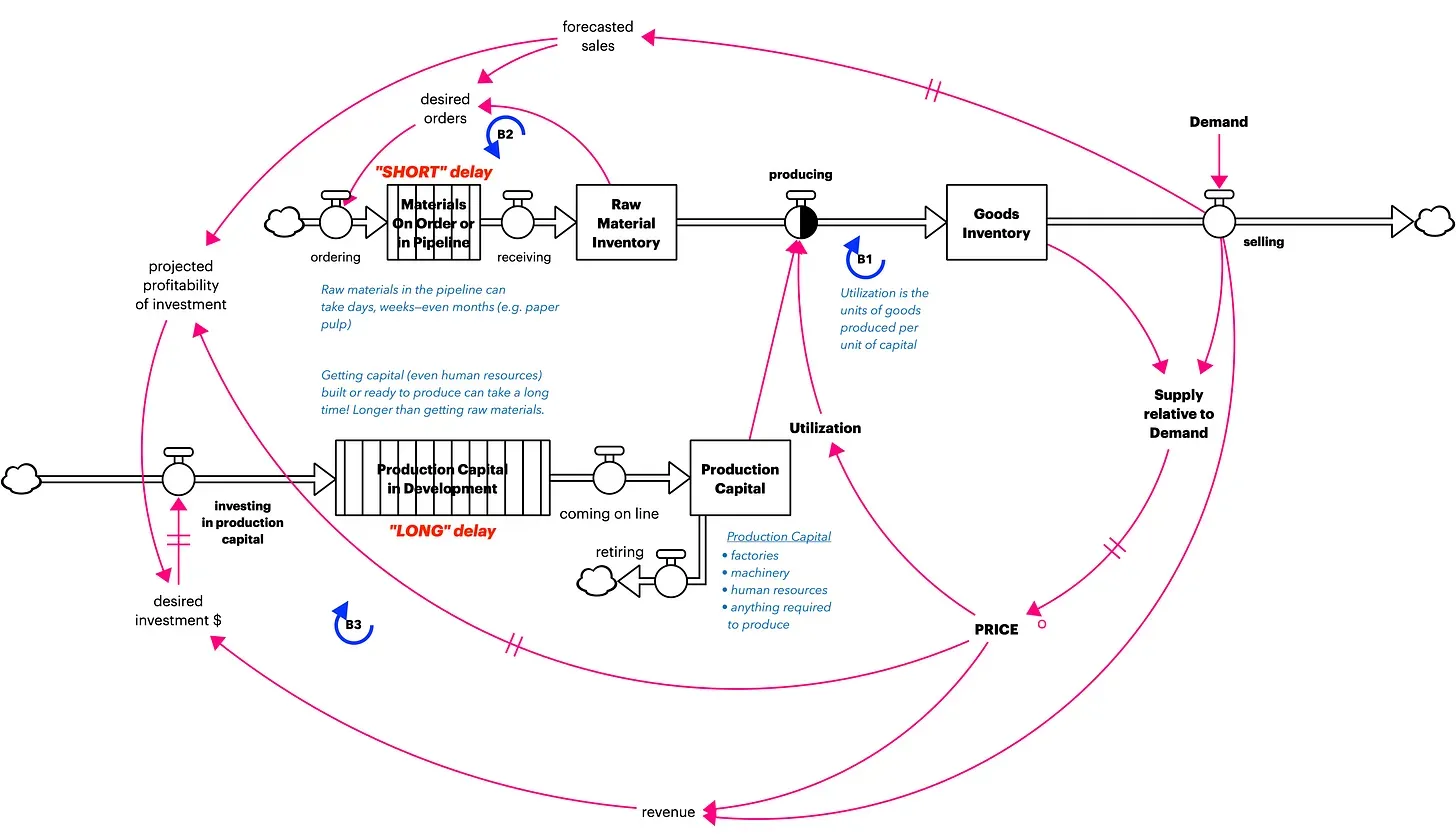

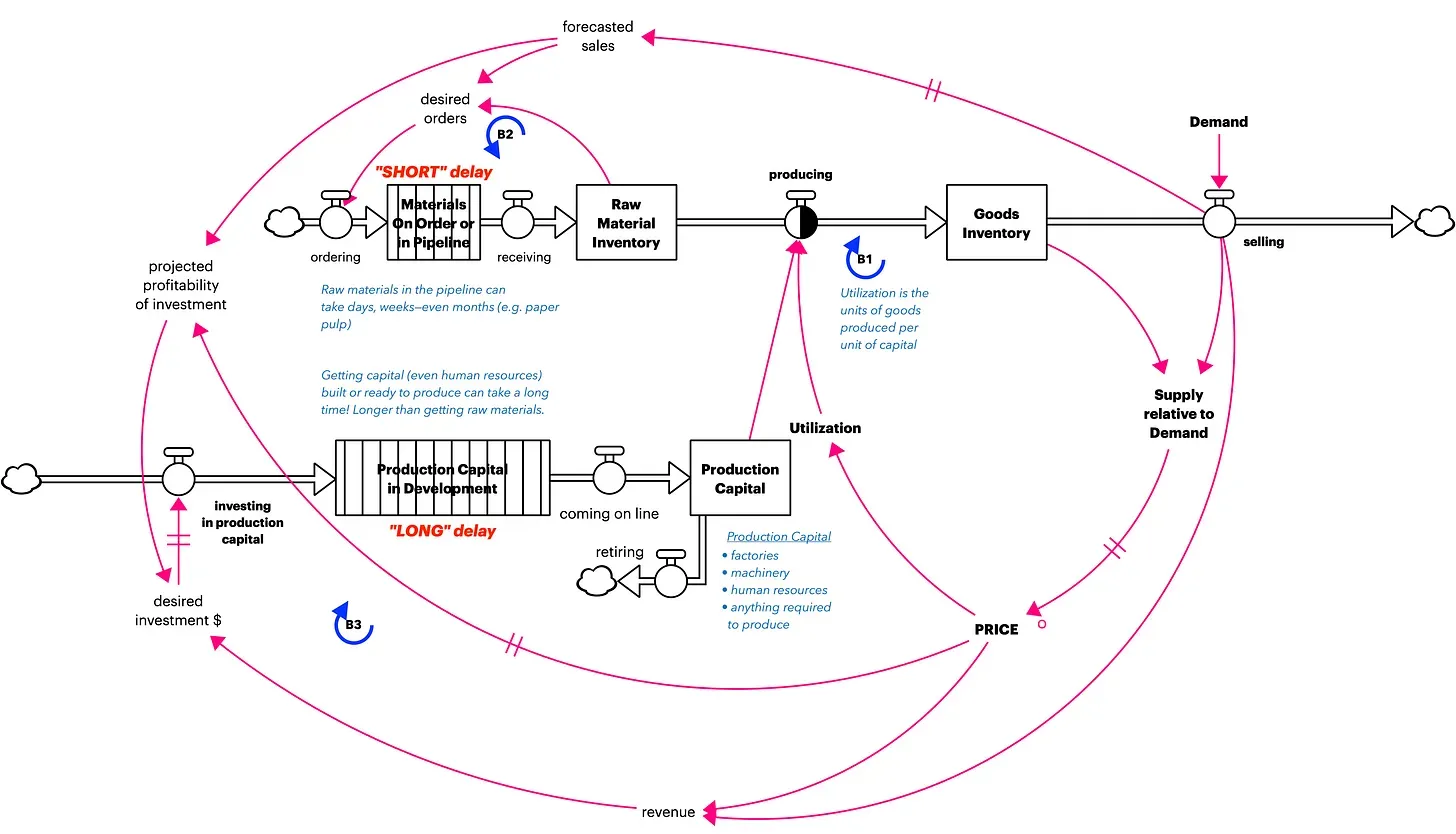

THE BASICS OF SUPPLY AND PRODUCTION

A 30,000 meter view of any industry might look like the map above. At any point in time, you can count up the current amount of goods in the Goods Inventory stock. The stock is like a bathtub. It accumulates inventory.

What fills it up each week is the amount of producing (production) that week. This inflow of producing is like the spigot into a bathtub. The valve (on top) determines how fast or slow the bathtub of Goods Inventory fills. On the outflow, Consumer Demand determines how much selling (inventory sold per week) occurs weekly. If Demand increases, the rate of selling goes up. Lower Demand reduces the rate of selling.

Bathtub physics dictate that Goods Inventory goes up anytime the rate of producing exceeds the rate of selling. The only time Goods Inventory decreases is when selling exceeds producing.

The B1 indicates a balancing loop. Balancing Loops try to maintain equilibrium. If Goods Inventory declines, Price rises, utilization increases, Goods Inventory bounces back…and Price decreases again.

INCREASING THE CAPITAL STOCK INCREASES PRODUCTION

Producing occurs from applying Production Capital. Production Capital is also a stock, because you can stop time and in that moment count up the total amount of capital available. The rate of producing (units of goods produced / week) is determined by Production Capital * utilization (units of goods produced / unit of capital / week). To produce more requires increasing either the amount of Production Capital or its utilization (productivity) of capital—or both.

The binary shading of the producing flow indicates that there’s not a 1:1 conversion of raw material units into units of goods. One computer (a good) requires thousands of parts (raw materials like chips, boards, wires, etc…).

When Goods Inventory is running low, and especially when Price is high and industry profitable, organizations will order more raw materials, increase utilization and/or invest in new capital.

NOTE: It’s often easier—and takes significantly less time—to increase productivity (aka utilization) than to add Production Capital. Adding capital usually requires a flow (activity) of investment in production capital. That capital then steps onto a development conveyor and doesn’t actually become available to produce for a while. Sometimes this time delay takes months.

SUPPLY RELATIVE TO DEMAND—>PRICE

If Demand increases, the rate of selling increases, drawing down Goods Inventory. The Supply relative to Demand falls; Price will increase.

A producer typically responds by increasing utilization (units of goods produced per unit of capital) in order to produce more, filling up Goods Inventory, and bringing supply and demand back into balance. Price usually stabilizes to previous levels. Sometimes, producers will invest in new capital to increase production. This requires a much longer time horizon in order to implement.

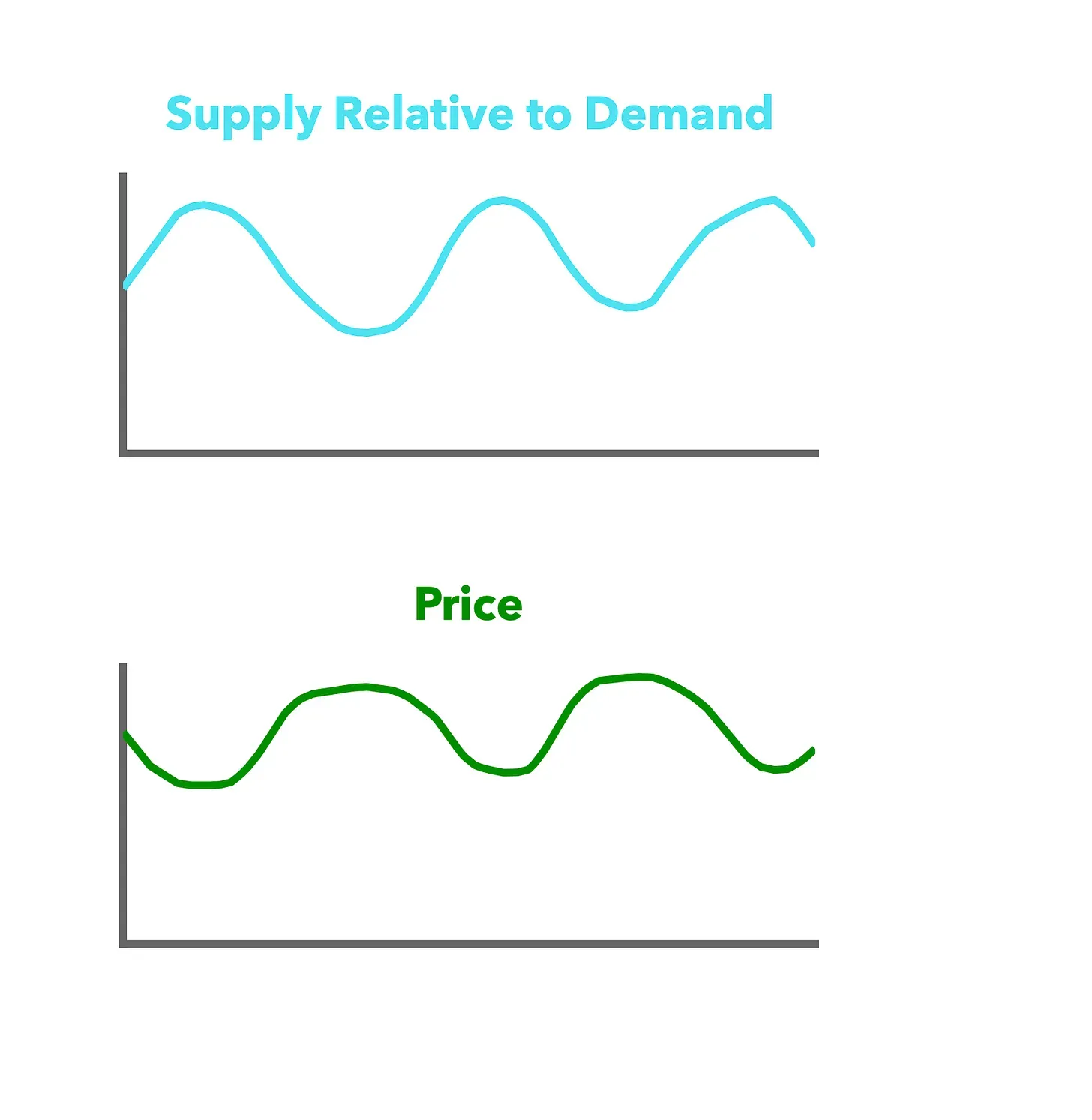

**WHY INFLATION? WHY SUPPLY SHORTAGES? AT THE SAME TIME?**

Under most situations, these balancing loops work to regulate the market so that production, inventories, and price oscillates around equilibriums—often with a little annual growth to create an upward sloping curve.

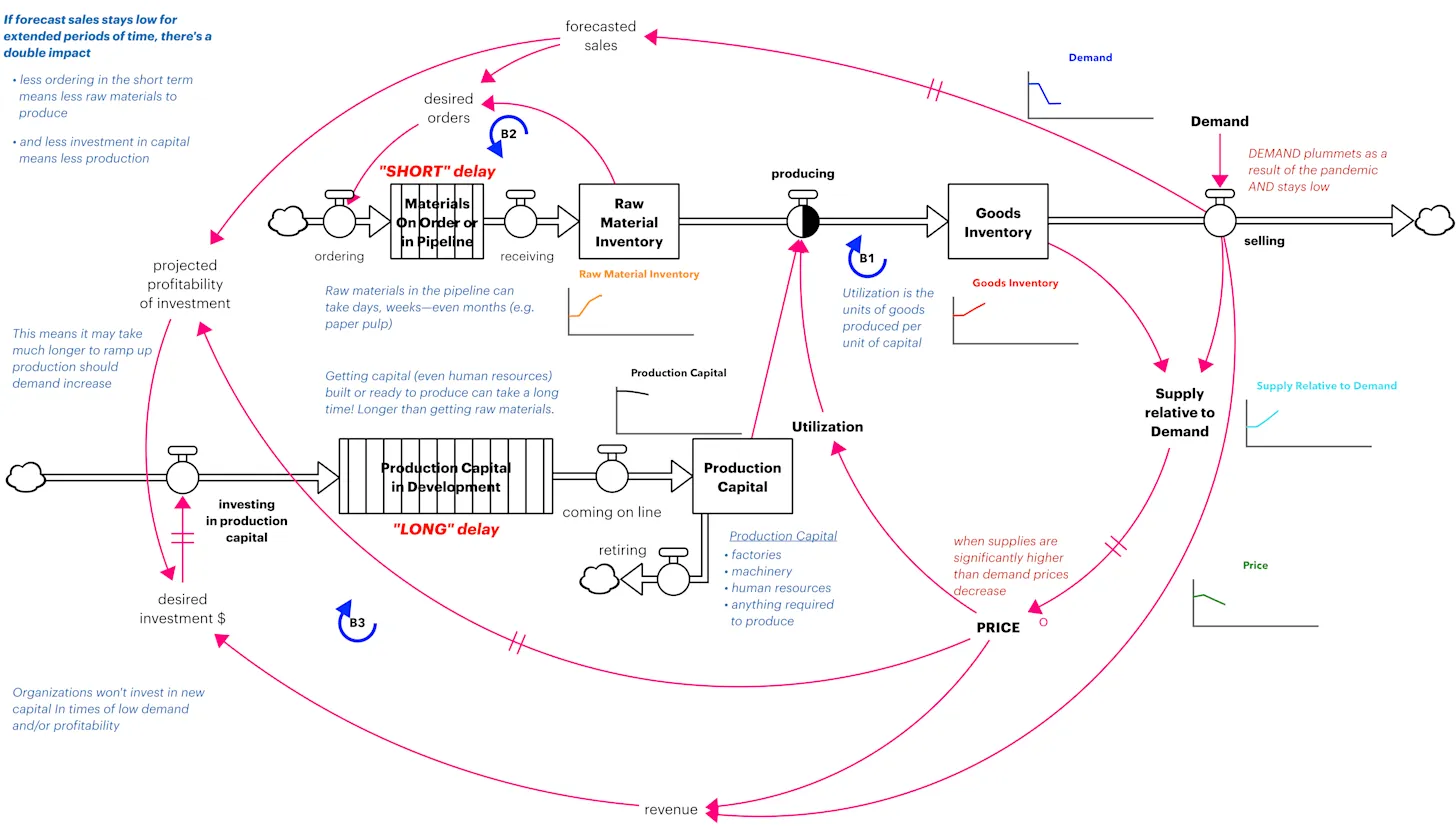

A Sustained Shock

But what happens occasionally are sustained shocks to a system. For example, if there’s a broad and sustained shock to demand (e.g. a lockdown), the following might occur.

Demand (blue trend) plummets and stays low. Supply relative to Demand begins to creep up (as unsold inventories increase). Too much supply causes Price to drop (or at least not increase anymore).

All of these reduce short-term utilization and materials ordering. This means less harvesting of trees, less of simple materials that are components to chips and computers, less of the basics. There will be less Raw Material Inventory (orange trend)

Further, Production Capital naturally retires, so the stock diminishes (or certainly doesn’t grow).

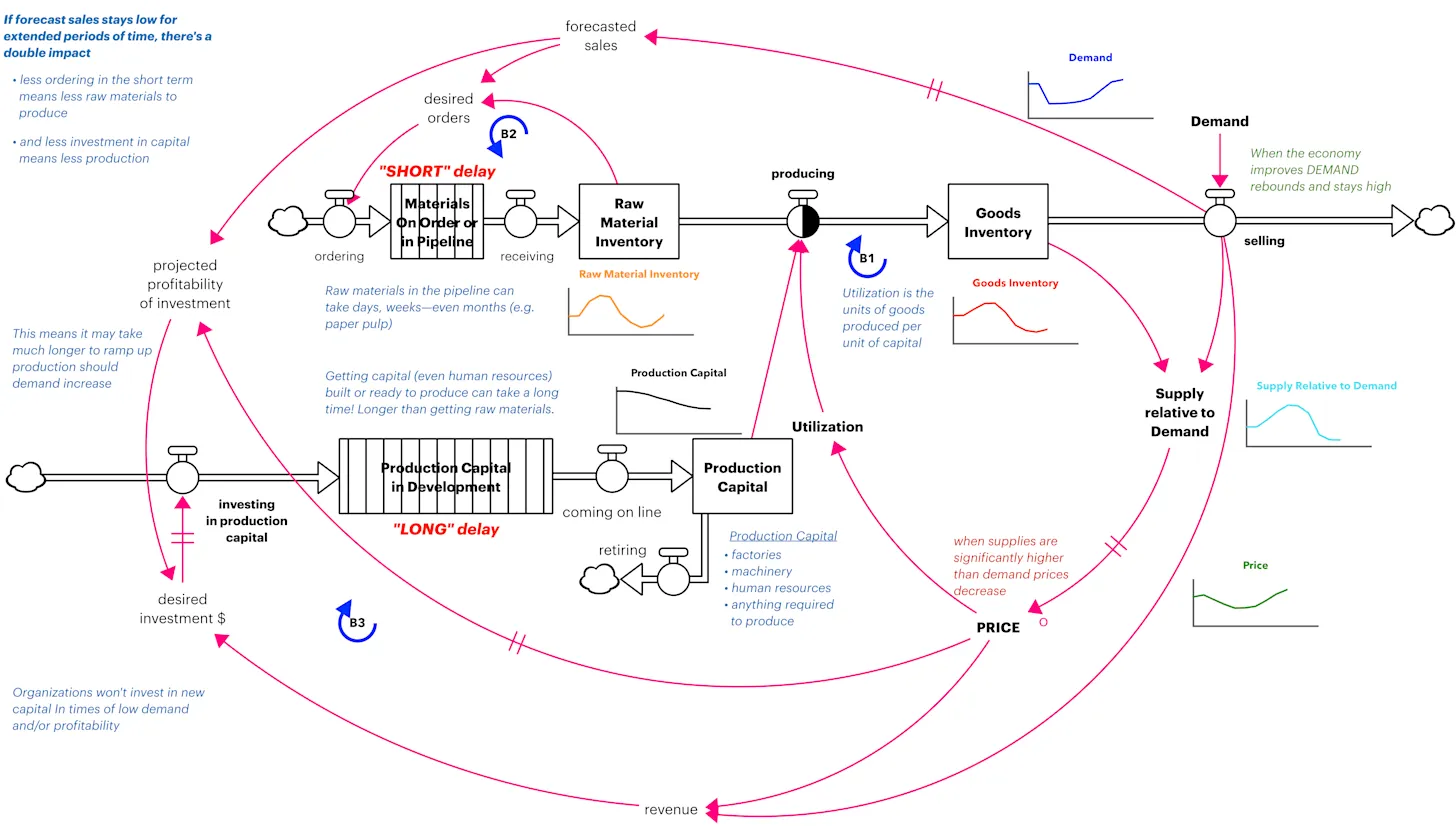

Demand Returns, But System Remains Behind

If Demand suddenly returns, the system can’t adjust back to normal immediately. Because Goods Inventory is now insufficient for this increased Demand, Supply relative to Demand decreases, and Price increases.

Utilization, ordering, and investing in production capital increases. But due to the long time delays—some delays are substantial—Price continues to rise as Supply relative to Demand remains low.

And INFLATION!

Inflation Continues

Inflation (increasing Price above wage increases) will continue for a long time as the system tries to recover…especially if Demand continues to remain high. The long pipeline delays ensure this dampening of inflation takes time.

Solutions?

What will address this shortage combined with inflation? The main national lever works on demand. The strongest lever is the natural one: Price—>Demand. Yes. Prices will eventually go high enough to naturally suppress demand. As selling slows, inventories can catch up, and Price will fall (or stop rising as fast).

Policies that could slow demand sooner might include short term taxes on some (perhaps luxury) items that require a lot of raw materials. This would increase actual Price faster than inflation and put the brakes faster. Plus, luxury items taxes wouldn’t negatively impact those suffering the most. And if the tax was reinvented in ways that increase the development of supporting infrastructure and capital, then the system would rebound faster.

Additionally, there could be incentives to industries to invest in capital even when their forecasts don’t encourage them to do so. Incentives to add supporting infrastructure or invest in employee development would pay off in the medium to short term.

IMPLICATIONS

What happened in 2020 was unique in that Demand was suppressed suddenly (lockdowns) and for a longer time than typically. This means that rising inflation now is absolutely to be expected. So, who’s to blame?

The current President wasn’t responsible for the 2020 sudden and sustained decrease in Demand. And the previous President, although a different way of handling the pandemic might have reduced the impact on Demand, isn’t responsible for the way the market is now responding to reinvestment to bring production back up to previous levels.

Key Insight

Today’s macroeconomic performance is rarely the result of decisions made within the past few months. Using a longer term mental model of the structure generating performance will increase our ability to assess any attributions of “who’s to blame?”